Savills’ Head of Research, Lucian Cook anticipates recent interest rate cuts will make it easier for borrowers to meet lenders’ affordability tests, thereby expanding the pool of potential buyers, reports Zahra Jawad

Savills’ Head of Research, Lucian Cook, has told the London Daily that he anticipates recent interest rate cuts will make it easier for borrowers to meet lenders’ affordability tests, thereby expanding the pool of potential buyers.

However, despite this optimism, the recent rise in inflation, which reached three per cent in January, has made both experts and buyers cautious. This is because lenders often price mortgages based on long-term expectations.

Therefore, if inflation is expected to remain stubbornly high, mortgage rates may continue to be elevated. In recent years, since the COVID-19 pandemic, the market ecosystem has experienced periods of uncertainty and turbulence, with base interest rates soaring well above pre-COVID levels.

The current rate stands at around 4.5 per cent, with Oxford Economics forecasting three further cuts in 2025, bringing the base rate down to 3.75 per cent by year-end.

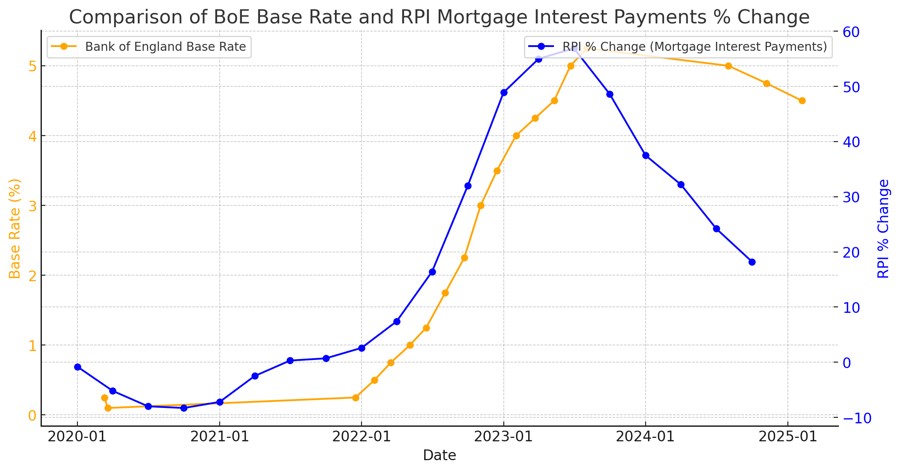

The recent 12-month percentage change in Mortgage Interest Payments saw a significant surge from 2022 to 2023, followed by a gradual decline in 2024. This trend closely mirrored the Bank of England’s base rate movements, as rising interest rates led to higher mortgage interest payments.

But despite the bank rates decreasing, mortgage costs stayed high even as interest rates stabilised. This is due to the lag effect, whereby the drop in bank rates won’t see an immediate effect in the mortgage interest payment, as it usually takes time for the market to react. Fixed mortgage rates remain the same until their tenure comes to an end.

Lenders may also be cautious of reductions due to uncertainty, prompting them to keep their rates up. As of February 2025, the BoE has reduced its base rate to 4.5 per cent. However, mortgage rates remain high at around 4.9 per cent (2-year fixed) and 4.72 per cent (5-year fixed), reducing by only a small amount compared to their peak in 2023.

During the interest rate surge that began in 2022, the BoE’s database showed that fixed-rate mortgages (up to 2 years) saw the biggest raw increase: from 2.24 per cent to 4.91 per cent (+2.67) from February 2023 to December 2024.

When looking back at the optimism Cook shows, the uncertainty that has haunted the UK economy may dampen the hopes the researcher exhibits. If history has proven anything, it is that uncertainty and unexpectedness have become the norm in today’s economic climate.

The Independent has stated that the next reduction rate may be pushed back as the BoE will now keep a close eye on inflationary pressures in the coming months. However, Cook may be right, as major lenders, including Barclays, HSBC, Nationwide, NatWest, and Santander, have cautiously begun to lower at least some of their fixed mortgage rates.

In February, Nationwide reduced its fixed-rate mortgage products by up to 0.35 per cent. But if inflation continues to remain stubbornly high, the falls seen could potentially go into reverse and end up being short-lived.

The next base rate announcement is due on 20th March, with the Bank’s governor, Andrew Bailey, saying the MPC would be “taking a gradual and careful approach to reducing rates further.”

Lucian Cook’s optimism will now depend on the broader economic climate, making the forecast a little more obscure than it initially seems.

ALSO READ: UK Front Pages 27/02: Political Leaders Urge US Support to Prevent Russian Invasion of Ukraine

ALSO READ: A Crisis In 22-Yards